Investors rotate toward certainty as President Trump seeks to reshape the economy

Key Observations

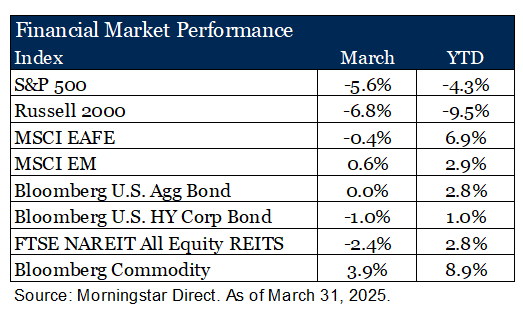

• U.S. Equity Selloff – The S&P 500 fell -5.6% in March and -4.3% for the quarter, its worst since 2022, as stretched valuations and concentrated leadership fueled volatility.

• Mag Drag – Despite 61% of securities posting returns better than the index, AI concerns and a selloff in high-valuation stocks pulled down the market. Six of the “Magnificent 7” fell between -11% to -36%, underperforming the S&P 500.

• Global Rotation to Stability – Investors shifted away from U.S. equities, favoring Europe and China. MSCI EAFE outperformed the S&P 500 by 11% for the quarter, its strongest lead since Q2 2002, while China gained 15% on stronger manufacturing data and renewed policy efforts.

• Growth Scare – The Federal Reserve is expected to hold rates, while fiscal policy tightens. Tepid consumer spending and declining confidence add to economic growth concerns.

Market Recap

Growing concerns over U.S. policy uncertainty, coupled with slowing economic momentum, triggered a selloff in U.S. equities. The S&P 500 declined -5.6% for the month and -4.3% for the quarter, marking its worst quarterly performance since 2022. As we highlighted in our 2025 Outlook, stretched valuations and heavy index concentration set the stage for heightened volatility

Beneath the surface, 61%1 of securities outperformed the headline index return, but the weight of the “Magnificent 7” proved too great. Profit-taking in these high-valuation positions, alongside AI-related concerns—such as Alibaba’s co-founder warning of excess data center capacity and reports of Microsoft pausing projects in the U.S. and Europe—weighed on sentiment. All Magnificent 7 constituents, with the exception of Meta, posted declines greater than the index, with shares down between -11% and -36% for the quarter.

This rotation reflects a broader investor repositioning, both by sector and geography, as market participants sought shelter from volatility. In contrast to the uncertainty gripping the U.S., European equities benefited from relative policy stability and slower headline-driven turbulence. With the U.S. shifting toward a more protectionist “American First” stance, Germany is in a potential new leadership position—both economically and in defense policy. German equities rallied 11% for the quarter, 15.5% in U.S. dollar terms, supported by a weaker dollar relative to the euro. Broader European markets also performed well, with the MSCI EAFE outperforming the S&P 500 by 5.6% for the month and 11% for the quarter—the largest quarterly outperformance since the second quarter of 2002 and the 10th best relative return since 19701.

Meanwhile, China rebounded, posting positive returns for the month and a 15% quarterly gain, driven by stronger manufacturing data and renewed policy efforts from President Xi to revive economic confidence. However, it remains early days in the U.S.-China policy shift and given that the U.S. remains China’s largest trading partner, geopolitical risks remain.

On the economic front, the Fed is expected to keep rates steady amidst rising policy uncertainty and inflation hovering slightly above target. However, fiscal policy shifts are well underway and moving toward austerity. As we discuss further below, with both major economic levers now in restrictive mode and tepid consumer spending (-0.6% m/m in January and 0.1% m/m in February2) and confidence throughout the quarter, the risk of an economic slowdown is rising. In response, interest rates declined over the quarter, supporting positive fixed income returns, though performance was flat for the month. Credit markets, while initially muted despite growth concerns, began to react, with high-yield spreads widening from ~260 lows in January to ~3501 by the end of March. As a result, credit underperformed for the month.

Trumpenomics

It would be seemingly disingenuous to discuss markets without addressing tariffs. They dominate headlines and fill our mental bandwidth with their unpredictability. However, we will avoid the temptation to chase the latest tariff headline and instead focus on the broader economic signals at work. To do that, we must first revisit the fundamental role of government in shaping the economy.

The U.S. government influences economic outcomes primarily through two levers: fiscal policy and monetary policy. Fiscal policy, dictated by government spending and taxation, directly affects GDP with government spending and indirectly effects consumption. Monetary policy aims to balance full employment and price stability by adjusting interest rates and money supply. Higher interest rates, for example, are used to curb inflation, while lower rates encourage borrowing and investment. So, what does Trumpenomics look like in practice? The administration is seeking a tight fiscal policy and loose monetary policy approach.

- Tight fiscal policy: The administration seeks to reduce government spending (e.g., DOGE) while increasing revenue (e.g., tariffs). In isolation and in the short-term, this would slow economic growth as the government spends less, reducing its economic impact, and consumption slows modestly, as Federal employees are without work.

- Loose monetary policy: Lower interest rates and deregulated banking would, all else equal, stimulate growth by encouraging consumption and investment.

The administration’s wager is that monetary stimulus will more than offset fiscal restraint, sustaining economic expansion with a more balanced budget. At a glance, it is possible—after all, government spending has accounted for ~20% of GDP since 2000, meaning a decline in public expenditures could, in theory, be counterbalanced by modest increased private sector activity that accounts for the remaining 80% of GDP3. But here is the rub: the administration only controls one of these levers.

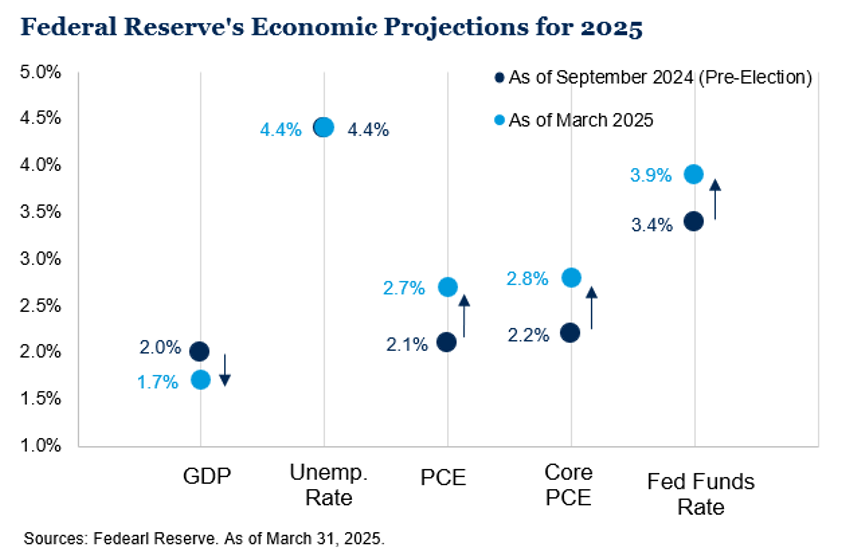

While fiscal policy falls under the purview of the executive and legislative branches, monetary policy is dictated by the Federal Reserve (the Fed). The Trump administration has moved swiftly to implement its fiscal vision, but the Fed is operating from a different playbook, as shown in the Fed’s Dot Plot below—which reflects projections from Fed policymakers. Collectively, Fed governs have shifted their view from pre-election (September of last year) to this March, predicting that growth will slow and inflation will raise, causing a slightly higher Federal Funds Rate. This suggests that Fed officials believe it prudent to maintain restrictive monetary policy.

Instead of the administration’s preferred mix of “tight fiscal, loose monetary,” we have “tight fiscal, tight monetary,” producing a restrictive economic policy stance. The disconnect has helped fuel the recent growth scare as an economic slowdown becomes an increasingly plausible outcome.

Outlook

Despite the seemingly rapid rate of change, our positioning outlined in Bridging the Divide for 2025 remains as relevant today as when it was published. A fragile market—characterized by high valuations, high concentration and the persistent risk of rising inflation—tilt the odds toward heightened volatility. Additionally, with the increasing likelihood of simultaneously restrictive monetary and fiscal policy, coupled with tepid consumer spending, the probability of an economic slowdown has risen. Considering we highlighted these risks coming into 2025, we believe our current portfolio positioning reflects our best current thinking given market conditions.

That said, it is important to remember that market volatility and economic slowdowns are a natural part of investing. As of March 31, the S&P 500 had declined 9.2% from its peak—a move that may feel unsettling but is well within historical norms. Since 1990, the average intra-year drawdown is 9.7%4 —nearly identical.

While periods like this may seem atypical in the moment, history suggests that staying focused on the long term remains the most profitable approach. Markets have a way of transferring wealth from those who react impatiently to those who maintain discipline and perspective.

1FactSet as of March 31, 2025

2Bureau of Economic Analysis Real Consumer Spending as of March 31, 2025

3JPMorgan as of March 31, 2025

4Morningstar as of December 31, 2024

Disclosures & Definitions

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses. Market returns shown in text are as of the publish date and source from Morningstar or FactSet unless otherwise listed.

- The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

- MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

- MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country.

- Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

- Bloomberg U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

- FTSE NAREIT Equity REITs Index contains all Equity REITs not designed as Timber REITs or Infrastructure REITs.

- Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification.

Material Risks

- Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

- Cash may be subject to the loss of principal and over longer periods of time may lose purchasing power due to inflation.

- Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

- International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impacted by currency and/or country specific risks which may result in lower liquidity in some markets.

- Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

- Private Real Estate involves higher risk and is suitable only for sophisticated investors. Real estate assets can be volatile and may include unique risks to the asset class like leverage and/or industry, sector or geographical concentration. Declines in real estate value may take place for a number of reasons including, but are not limited to economic conditions, change in condition of the underlying property or defaults by the borrower.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.