A look back on the QDIA landscape in 2024

Qualified Default Investment Alternatives (QDIAs) have solidified their position as a cornerstone in today’s retirement plan landscape. Like recent years, 2024 was another year of progress and evolution in the space, with several notable developments and trends that may shape its future trajectory.

Target Date Utilization

Global retirement assets (pension & defined contribution) reached an estimated record high of $58.5 trillion in 2024, including $26 trillion of defined contribution assets in the United States.1 Target date solutions continue to be preferred by an overwhelming majority of Plan Sponsors, serving as both the most common default offering and the largest recipient of participant cash flows in investment menus. Target date funds are the QDIA in 98% of plans, according to Vanguard’s How America Saves 2024 report, a figure that has remained consistent over the past five years.2 This fact, combined with a tailwind from capital market performance that saw broad-based equities rise, resulted in global target date asset levels continuing to increase in 2024.

Target date trends we noted in the 2022 and 2023 versions of this report persisted throughout 2024. Passive target date solutions continued to garner the majority of flows and Commingled Investment Trust (CIT) vehicles continued to gain popularity. While passive solutions typically have lower expenses compared to fully active or blend/hybrid counterparts, it is important to recognize that active decisions are made in any target date solution for the determination of the portfolio objectives, strategic asset allocation and underlying building blocks.

CIT vehicles continue to attract interest within the institutional investing industry, in part due to their potential for lower and more flexible fees, but also due to improved transparency and reporting that has occurred in recent years. These trends have led to wider adoption of CITs, not just for target date funds, but across all investment offerings within the retirement landscape. Increased rates of CIT adoption was perhaps most pronounced in 2024 among plans in the smaller end of the market, in part due to greater education and comfort with these vehicles, combined with decreasing investment minimums imposed by money managers and trust companies.

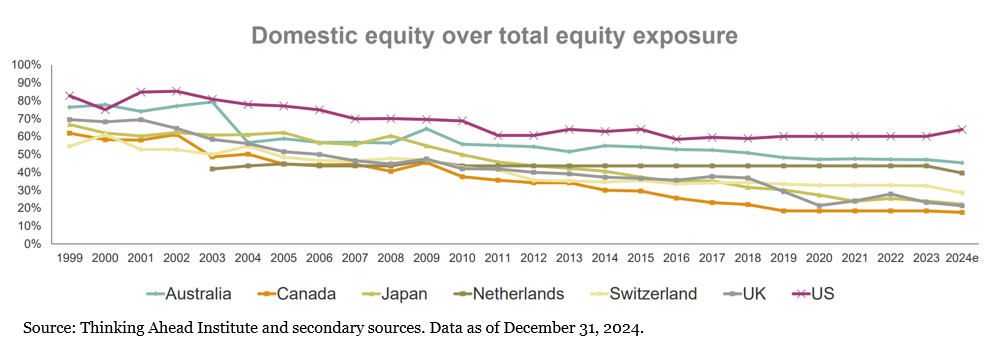

We Are Going Global!

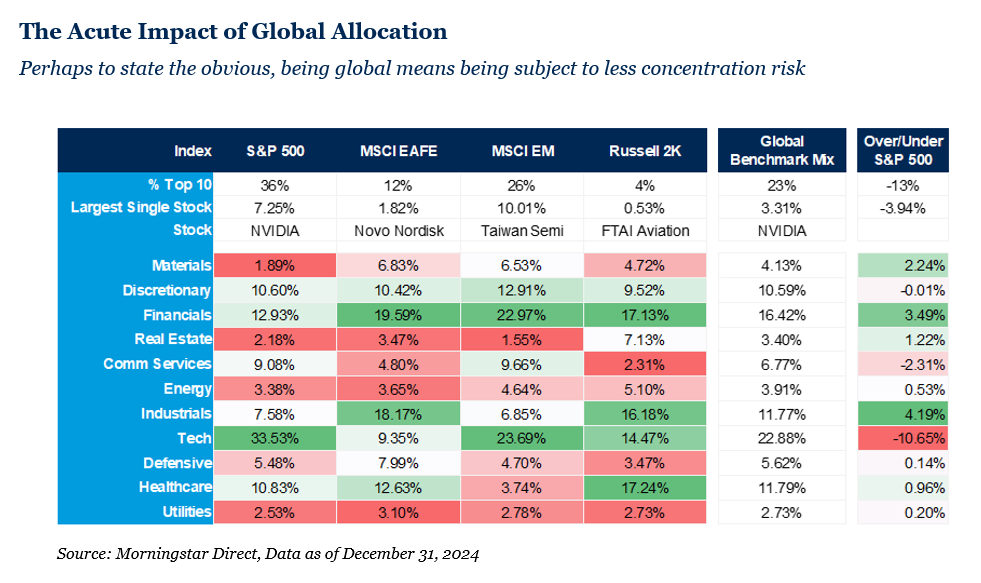

Since their creation, target date funds have offered exposure to both domestic and international equities, but generally with a “home country” bias versus the global equity market capitalization. Despite international securities broadly lagging domestic counterparts in recent years, an observation among solutions in 2024 was an increase in the non-U.S. exposure. This aligns with a trend occurring in retirement plan investments globally for the past few years.

Many providers have changed their strategic asset allocation in recent years to increase international exposure, most notably among equities, but to a lesser extent within fixed income as well. Anecdotally, rationale provided by money managers on this development falls into two primary buckets:

1. Current market valuations and relative capital market assumptions

2. Improved diversification and potential risk reduction in a concentrated domestic equity market

Near-Term QDIA Proposals

In 2024, the ERISA Advisory Council (EAC), an advisory body that advises the Department of Labor (DOL) on ERISA topics, discussed and introduced potential proposals involving the QDIA space. The EAC approved some of these for recommendation to the DOL in December, including guidance of decumulation and annuities in QDIA solutions as well as the potential for QDIAs for involuntary rollovers.3

Guidance – Similar to the target date selection and monitoring guidance that the DOL provided in 2013, one of the 2024 proposals involves establishing guidance or a “tips sheet” for fiduciary committees in selecting a decumulation or annuity offering. The intent is to establish a prudent process for selecting a lifetime income QDIA option, to assist Plan Sponsors with mitigating litigation risk, currently viewed as a leading roadblock to the adoption of lifetime income options as QDIA. This guidance may be material in providing Plan Sponsors greater comfort on incorporating annuities more broadly into their plan offerings and is likely to be similar to the Interpretive Bulletin (IB) 95-1 which provided considerations for fiduciaries when choosing an insurer/counterparty for pension risk transfer.

Involuntary Rollovers – The EAC has also proposed that the DOL review the current QDIA options for IRAs and more specifically, involuntary rollovers. In some cases, Plan Sponsors may roll a participant’s balance in the defined contribution plan into a safe harbor IRA, provided the participant balance is below a certain threshold (currently $7,000). In practice, the money is most often placed into a cash equivalent offering, which might lack the growth potential that could benefit participants. This approach differs significantly from defined contribution plans, where nearly 98% of all 401(k) Plan Sponsors designate target date funds as the QDIA, according to Vanguard’s How America Saves 2024 report.4 In the recent proposal, QDIA safe harbor provisions would apply to other investment types, not dissimilar to those that are currently available in defined contribution plans (target date funds, managed accounts, balanced funds). This recommendation is one that Vanguard’s Policy Research group also made via a research paper earlier in July 2024. In this report, Vanguard comments that IRA cash is highly “sticky” and that “enabling an IRA qualified default investment alternative (QDIA) could deliver approximately $172 billion in long-term benefits to all rollover investors in retirement each year.” While the number of participants in IRAs is lower, the asset figures of IRAs is greater than that of defined contribution plans, meaning the implications from a QDIA change could be material for money managers.

Closing Thoughts

The developments in 2024 QDIA solutions highlight the ongoing evolution of these investment options. Additionally, the strong market appreciation in 2024 has provided a tailwind for their asset levels, further solidifying their position within plan menus and target date’s position as the most common QDIA structure in the industry. In addition to the developments cited, other trends worth monitoring include the increased popularity of blended active/passive strategies, the emergence of personalized solutions and the inclusion of income-oriented solutions; all of which are likely to contribute to the dynamic landscape of QDIAs.

In the nearly 20 years since the Pension Protection Act paved the way for QDIA adoption, they have arguably grown to be one of the most important developments in the retirement industry. With ongoing advancements and improvements expected to enhance their effectiveness further, these investment solutions will potentially play a crucial role in helping participants achieve their financial goals and secure their financial future. By staying informed and making strategic decisions, Plan Sponsors can maximize the benefits of QDIA offerings. As Plan Sponsors and participants continue to navigate these changes, the importance of prudent evaluation and selection of QDIA and target date funds remains paramount.

To discuss your QDIA offering or any of the topics discussed within this paper, please contact the professionals at Fiducient Advisors.

1Global pensions assets climb to record USD 58.5 trillion – Thinking Ahead Institute

2How America Saves Report 2024 | Vanguard Institutional

3DOL Discusses Reforms to QDIAs: Annuities, Rollovers, and Litigation, October 29, 2024

4How America Saves Report 2024 | Vanguard Institutional, December 31, 2023

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.